Minister for Finance Paschal Donohoe

This afternoon.

RTE’s News At One broadcast an interview Christopher McKevitt had recorded earlier with the Minister for Finance Paschal Donohoe.

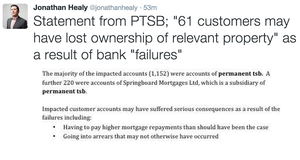

They discussed Permanent TSB’s plans to sell loans connected to 14,000 private homes in Ireland.

From the interview…

Paschal Donohoe: “The board of Permanent TSB can and have moved ahead with this process and do not require my consent to do so.”

Christopher McKevitt: “And yet many people will say that, as the Minister for Finance, you wield extraordinary power and you wield immense power over Permanent TSB in particular amongst banks because you own 75% of the lender on behalf of the Irish people. So, setting aside the many pressures that you’re under, in order to restore a healthy banking system and protect people in vulnerable situations in mortgage difficulties, what do you intend to do or what can you do?”

Donohoe: “And I’m privileged to be in this office and I’m deeply aware of the concern and vulnerability that many people feel as a result of the announcement by Permanent TSB but I also have to be conscious is we have a Central Bank regulator that is saying to Permanent TSB that it needs to reduce its non-performing loans and the bank that we are talking about in Permanent TSB has a million customers and it has deposits of €17billion and it’s essential for the long-term health of Irish banking that we have a third bank that is sustainable and is secure. As against that, of course I appreciate the concern that people feel about this announcement and that loan owners in particular feel and I’m really, acutely aware of that.”

McKevitt: “Because many would feel that this is perhaps a soulless, cost accounting exercise lacking completely in compassion and that’s where you step in, that’s your role.”

Donohoe: “And I would relate that back to all of the experiences that we have had over the last number of years in relation to Irish banking. We have a legal and regulatory framework in place that has been allowed and seen the amount of mortgage arrears in our country decrease very, very significantly so, for example, Permanent TSB has halved the mortgage arrears they have from around 33,000 cases to 16,000 cases.

“We’ve managed to see this kind of change happen with a low level of home repossessions to date. And the reason why those things have happened is, as against the figures, which I’m deeply aware of, I’m also aware of the social cost and difficulties involved in this kind of change happening.

“And that is why, as I look to deal with this matter, across the coming months, yes it is vital that we have a Permanent TSB that it’s in a long-term, stable and sustainable [inaudible] I want that to happen. We all need to see it happen. I also cannot be in a position that I’m interfering with how a Central Bank works. We put that behind us.

“And I want to create and build on having an environment in which people are treated fairly and effectively as this moves forward.”

McKevitt: “But yet you say Permanent TSB has done good work in reducing the number of loans in mortgage arrears. What’s the problem with continuing that work in much the same vein as they’re going? They’re talking about a sum of €3.7bn attached to 18,000 properties – 14,000 of those are private, principled dwelling homes for people who have families presumably, people who are embedded in their community, requiring schools and services.

Donohoe: “With respect, I didn’t say that good work had happened here, because I’m conscious that as that work happened that it was also very difficult, it involved lots of difficult conversations with citizens. To answer your question directly about why they are required to do more, they’re required to do more because they’re non-performing loans, as a percentage of their balance sheet are at 28% which is five times the average across the Eurozone.

“And I’m conscious as I say that to you Christopher and your listeners that they are figures against the worry that people feel today. But reducing those figures today is vital to ensuring that we have a stable and competitive banking system in the future, able to deal with the next difficulty that we might encounter. And what I will do in order to deal with the concerns that I know have been ignited by this announcement is I will look at the legal and regulatory framework that we have in place afresh. It will be an opportunity to do so as a minister for finance dealing with this matter. And I will be asking and consulting with the Central Bank for their further views on where they stand today.

“And I will be meeting deputy Michael McGrath this afternoon to look at how I can engage constructively in his bill and I’m going to do all of that because as we make the journey to having a stable and secure banking system and further work needs to happen there, I do so conscious of the worry that people feel now and the misery that we’ve already gone through. And I want to ensure we have the fairest legal system in place to balance all of that together.”

Later

McKevitt: “It sounds like there’s quite a job of work for Fine Gael and Fianna Fail and I’m thinking confidence and supply here to do, in order to have a meeting of minds.”

Donohoe: “And. Permanent TSB have reduced their mortgage arrears by 43% versus the peak difficulties we were all in. So one of the points, they had 33,000 families that were affected by this, it’s now nearer 16,000. If you look at where we are, as an entire country, a few years ago, we had €54bn worth of loans that were classed as being non-performing loans – that figure is now €22bn so a journey has been made but for a bank in particular they still have a level of non-performance that is exceptionally high by either regulatory or European average.

“And what I will be doing is I will be meeting deputy McGrath this afternoon. I understand the concerns that he is raising and I will be working constructively on that bill to see how it can be adopted, how we can build on it and then, in parallel to that, I will be consulting with the Central Bank to take account of where we are now and where we might go to the future.”

McKevitt: “Are you happy that of the order of 18,000 property loans will shift potentially, and many say very likely, to an investment fund outside the gaze and outside the control, the regulatory control of the Central Bank of Ireland?”

Donohoe: “Well, if I could break that into two different questions. Firstly, in terms of who will buy and what will be bought, I genuinely can’t answer that question today Christopher and the reason why is this process has not yet even begun to get into that area.

“So later on in the year, Permanent TSB and then I will be able to answer that question but I can’t do so today.”

“In relation to the second part of your question. Any organisation who is managing the loans on behalf of a private fund who might not be located in our jurisdiction is already regulated. So that regulation is in place and the rights that anybody will have and does have will not be changed by the change in ownership of the loan.”

McKevitt:“And you’re referencing the Credit Servicing Firms Act of 2015 but that act does not include determining the overall strategy for the management and administration for those portfolios of loans – the making of portfolio decisions or enforcing indeed loans. So, in a sense, there is still many would argue, far too much free rein for what people call vulture funds to do as they please with the lives of fellow citizens.”

Donohoe: “And as against that, before I answer you question and tell you what I’m going to do about it. Against that, let’s just be cognisant of the journey that has occurred in relation to non-performing loans and banks within our country where we have a legal framework currently in place that has seen many of these difficulties evolve and be resolved without the mass home repossessions that did appear a prospect in our very very recent past.

“But then to answer your question regarding where we are now – that’s why I want to be very clear with your listeners on this matter. The legislation that was in place happened in 2015 and I will look at this issue afresh both by asking the Central Bank for their views and where we stand now and then by engaging with Deputy McGrath and his party on this point across the coming weeks and months.”

McKevitt: “Briefly, can we look at what Permanent TSB has told us about the portfolio, the Project Glas portfolio it’s selling. It’s loan values of around €3.7billion, 14,000 of them principled dwelling homes, they’re saying €1bn of the €3.7bn is investment properties and the remainder then is principled private homes. Of that, they’re saying close on €2bn worth of those loans with principled private properties are people who haven’t engaged with the banks for a number of years. Do you feel that the time has come for those people to leave those properties if they haven’t engaged, if they’ve no entitled to maintain the property that they’re in.

Donohoe: “The recent trend and what we have managed to deliver in our country of people staying within their homes while difficulties being resolved as fairly as possible I want to maintain. I am so conscious of, particularly with the housing difficulties that we have of the value and necessity of having a stable home, a roof over your head – these things are a vital part of what it is to be a citizen. And a member of our state at the moment.

“In relation to the question that you have asked me about all of those loans, I want to maintain that approach but the answer is going to vary loan by loan and that is why I’m saying to you today that the legal framework that we have had replaced has been successful in staving off the kind of repossessions that many feared would happen and conscious of the concerns that have been ignited by this, I will look at that legal framework again.

“But the balancing act I have to manage Christopher, that’s why I wanted to talk to you about this issue today, is I have to work with everybody to weave a way through, having a stable banking system for our country in the years to come, able to lend to people, able to offer good rates of interest and deposit, able to offer security to people, while at the same time, deal with difficulties that are there and I am committed to try and find an build on a framework to do that.”

McKevitt: “Just north of €700m of those loans are people who have engaged with Permanent TSB, who have sought resolution and to discuss their mortgage arrears difficulties, should they be surprised that they’re going to be included in this tranche for sale?”

Donohoe: “Well, in, where that matter will move to is the legal rights that those loan owners have will not be changed. So they will have the same protection and obligations now legally – they will have the same level of protection in the future as they have now. So that is where they will stand in the future and it’s just an example of the kind of understandable sensitivity that people have here in relation to this transaction and that is why I”m being very clear Christopher, that the legislation that we have in place, I believe has served our country in dealing with difficulties that we had in the past and I will look at that afresh now to see how we can be best placed to manage the challenge that is approaching us now.”

Listen back here in full

Earlier: ‘A Sick Joke’

Tuesday: Michael Taft: Not Too Late To Save Public Banking

Noonans love child will sssssing off his masssterss hymn sheet.

Stooge

…the banks will be eternally grateful…well, maybe not eternally…or grateful…

How many people, in total, would be effected? Is that 14,000 families? More? Less?

By Christmas that number will be 36,000

And the amount in total, all people affected, including children, dependents?

So, 14,000 families who:

“…have not engaged with the Bank for over 7 years and on average the loans are over 3.5 years in arrears. Many have made no payments at all for years”

– will no longer be able to live in these houses for free. The houses can then be used to house 14,000 families who would not have somewhere to live otherwise.

While it is sad for the people losing their homes, you can’t just stop paying the mortgage and continue living in the house; eventually the bank will come and take the house back.

nice error and omission !

“some account holders have not engaged with the Bank for over 7 years and on average the loans are over 3.5 years in arrears. Many have made no payments at all for years.”

its ‘some account holders’-how many?-the minister knows or can ask-its simple math which TSB has and should be made available.

what does ‘many’ even mean-they are in charge of selling billions of loans for the state,resort to using terms like ‘many’ as opposed to the actual number,which they have !

why are they involved in a disinformation campaign-who’s instructing them ?

I agree:”some”&”many”are vague descriptions,what can’t the bank give exact figures?

Were any of these moved from tracker mortgages or put on the wrong rate?

What engagement did the BANK have with the customers?Was “rent to buy”options etc put forwards from the bank to the customers?

Fine – “on average … 3.5 years”

The point still stands: people who have not engaged with the banks and have lived for free for 3 years should not be rewarded with a free house.

Siding with the banks and foreign millionaire speculators against 14,000 Irish families. Rob, you are genuinely disgusting.

Who are ‘the banks’?

Here’s a clue: taxpayers

Taxpayers don’t get paid salaries and performance related bonuses from these institutions and don’t have an influence over their decision making, so to say that taxpayers are “the banks” is in no way close to the truth.

When people don’t pay their mortgage for 2 or 3 or 4 years to a state-owned bank, it is the taxpayer that they are not paying. When the same state-owned bank sells those mortgages for pennies on the euro to a vulture fund, it is the taxpayer who has just made a loss.

Taxpayers very much are the banks.

Well if the houses are repossessed and sold Tim, a different 14,000 will benefit. The former 14000 will have to start funding their own accommodation again.

Paschal should stop literally looking down his nose when he does these announcements.

And….. stop starting his sentences with ‘and…’

And….not be given the benefit of knowing the questions, as he was reading from a prepared script today.

How does it make any sense at a time when so many families are housed in “emergency” accommodation to add possibly thousands more to the list of people seeking housing? Surely its possible to think outside the box for once and come up with a solution that isn’t always focused on the needs of the market.

I don’t fully understand why these people aren’t allowed downsize. There is no end of families (currently stuck renting small apartments) who would be willing and able to pay for a mortgage in many of these cases.

Who would lose out in this scenario?

Where would they downsize to? It would be far easier to keep them where they are and figure out a way to make it viable for both sides.

So, if you buy a 5 bedroom house, don’t pay the mortgage for 3-7 years, the consequences should be… keeping the 5 bedroom house.

Madness…

Whats your solution?

These are loans that have not had any repayments in years, get these thieves out !!!

Some are.

why do they keep pushing this nonsense that borrowers who owe 2 Billion have not engaged,significant due diligence was completed in prepping the portfolio,the exact numbers are know,so why not be exact about it !

“Of the remaining €2.7 billion in loans, just under €2 billion is accounted for by PDH loans which are typically owned by customers who have not engaged with the Bank, whose mortgages are unsustainable or who have been unable to meet the terms of various treatments put in place. Of this portion of Project Glas, some account holders have not engaged with the Bank for over 7 years and on average the loans are over 3.5 years in arrears. Many have made no payments at all for years.”

http://www.permanenttsbgroup.ie/media/press-releases/2018/20-02-2018.aspx

2 billion comprised off borrowers who have not…

engaged with the Bank

mortgages are unsustainable

unable to meet the terms of various treatments

NOT (from above)

” Of that, they’re saying close on €2bn worth of those loans with principled private properties are people who haven’t engaged with the banks for a number of years.”

Can someone ask the Minister for the real numbers as they are available !

anyone have a guess on how much the blushirts will get for keeping their vulture fund mates happy?

…why don’t you ask your glorious leader Howlin…not so long since he was inside the tent…

Its not credible14,000 have lived in their mortgaged houses without paying a bean in over 3 years.

Are you saying that you don’t believe that the number are accurate? (i.e. that is fewer than 14,000)?

Or that it is crazy that the banks can’t evect someone that hasn’t paid a penny on 3 years?

the latest central bank stats show 31,624 in arrears for over 2 years, this sale accounts for almost half those ?

the numbers are deliberately vague and misleading,to feed a narrative of reckless borrowers that won’t pay and won’t enage,the numbers bandied about are not credible.

https://www.centralbank.ie/docs/default-source/statistics/data-and-analysis/credit-and-banking-statistics/mortgage-arrears/residential-mortgage-arrears-and-repossessions-statistics-september-2017.pdf?sfvrsn=5

The recession and bailout, 100% mortgages all come into play. Didn’t house prices dramatically fall, and thousands of tradesmen loose their livelihood? This could account for arrears and affected families. There will be chancers but 14,000 ? Can’t see so many families that irresponsible.

I have zero sympathy for people who are not paying back martgage payments. I presume that’s what non-performing longs means. If people were paying their mortgage then the bank would have no trouble with them. I would think the banks should be able to either kick them out, or else threaten them that if they don’t pay up they will be thrown to the wolves of the vulture funds – I guarantee they won’t take any shit from those strategic chancers. As a mortgage payer who has had to pay back monthly nearly a grand since 2004 on my own, it makes my blood boil to see these chancers getting away with paying nothing and basically living with free accomadation. Like to see them ever get another mortgage either after they get kicked out, zero chance.

+1

well said

disgusting treatment of the irish citizenry again.

It’s Trump talk “many many”. They’re offloading customers who are engaging & paying but have some arrears, have no doubt about it.

And isn’t it amazing that we have a minister for finance saying he can’t interfere in the the governing body over Irish Banks.. almost like a minister for justice saying she can’t interfere with the guards.

Im sick of these useless fupping gob sh*tes screwing ordinary people over.

They’ll interfere in the market bailing out wealthy investors and then say we can’t interfere in regulating them…WTF. Moronic stuff.

When will “the long-term health of Irish banking” mean that banks behave as I hope you would behave to me and I would behave to you? This grinding-out of profit from ordinary people and their homes is not good for our country.

And who believes a word out of the mouths of the current generation of bankers, when we remember their own accounts of sniggering behind the backs of the government regulators during the crisis of 2008 and “pulling figures out of their ****”?

We need a new, sensible model of banking in Ireland: we need to separate the kind of banks that lend to big business from the kind where people borrow to buy a home.

+1