From top: Minister for Finance and Public Expenditure & Reform, Paschal Donohoe and Taoiseach Leo Varadkar TD outlining to the media the update on Ireland’s Debt Service Costs outside Government Buildings last September; Michael Taft

There are a number of reasons being put forward to justify limiting the amount of budgetary resources available for repairing the social and economic damage of the recession years: an over-heating economy, limited fiscal space, future uncertainties.

One more reason is the level of government debt, as in ‘we have crippling levels of debt’ and we have to do ‘something’ about it (i.e. suppress government spending).

On first glance, our debt levels appear relatively modest. In 2017, our debt was 68 percent of GDP compared to a Eurozone average of 87 percent.

By 2021, the Government projects our debt to be 59 percent. This falls below the Fiscal Rules threshold (60 percent) which means our fiscal space expands; i.e. we’re allowed to borrow even more.

So far, so good. However, measures using GDP are not so good for familiar reasons. Therefore, analysists have been using GNI*, the CSO’s measurement which attempts to filter out distortions in our national accounts.

When we do this, a different picture emerges.

It’s been quite a toboggan ride. Irish debt was well below Eurozone levels in 2000. It fell even further up to 2007 though this was a period of speculative-based growth.

Between 2007 and 2013 debt went out of control – rising from just under €50 billion to over €200 billion thanks to a lethal mixture of collapsing tax revenue, falling output, bank debt (especially Anglo-Irish) and austerity measures.

However, since then the debt ratio has been falling.

By 2019 Irish debt will still be above Eurozone levels but not by much. Out of the 19 Eurozone countries, Ireland ranks mid-table in 8th place.

However, there are other measurements. For instance, Ireland fares poorly when we measure debt on a per capita basis. In the Eurozone, debt is €28,700 per capita while in Ireland it is over €43,000 – though one must take note that Eurozone per capita income is low compared to Irish standards. When incomes and prices are factored in, the difference could be reduced by half.

Another take on this ‘fiscally frightening the children’ scenario is the claim that we are still borrowing, still running a deficit. This, however, overlooks a key metric.

Looking at our current, or ‘day-to-day’ spending (this excludes capital spending) we are running a considerable surplus. In 2018, the Government project our current budget to be €4 billion in surplus, or 1.9 percent of GNI*. This will rise to over €8.1 billion by 2021 or 3.3 percent of GNI*.

In effect, we are running a considerable surplus on our day-to-day spending, the remainder being invested in our future infrastructure and growth prospects.

All that being said, there should be some concerns, not only because of the future uncertainties.

The classic approach to fiscal management during economic cycles is to reduce debt levels during periods of upswings while at the same time taking measures to ensure the upswings don’t get out of control.

However, such was the damage during the last bout of recession-cum-austerity; we need the extra expenditure for repairs. The big question is whether there will be enough time to finish these repairs before the economy enters into cyclical decline.

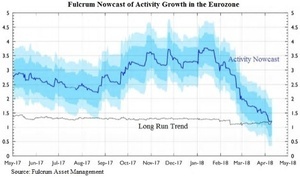

This question has gained some urgency with the recent and mysterious slowdown in Eurozone growth. From a big pick-up in 2017, Euro countries have started 2018 poorly.

The following graph comes from Fulcrum Asset Management showing not only a fall-off since the New Year but a continuing anaemic long-term trend. With UK activity hitting the doldrums it would be unwise to think Ireland will somehow escape.

This is not suggest that a recession is around the corner (but who knows given the near universal failure to predict the last one), but it does mean we have to do two things in preparation.

First, prioritise expenditure to strengthen the productive economy. The Government has started taking positive steps in this regard, increasing investment but it is crucial that we obtain value-for-money and that cost-benefit analyses are openly and thoroughly scrutinised.

We need to take further steps by increasing R&D expenditure (an area Ireland fares poorly in), introducing affordable childcare which can reduce barriers to labour force participation, and taking a more directive role with banks under state control to counter their intrinsic pro-cyclical character (that is, banks reduce their lending when it is needed most – during a downturn).

Secondly, we need to start recession-proofing the economy. Introducing pay-related unemployment benefit will help stabilise demand during a downturn while designing an employment subsidy scheme to keep employees in work by subsidising reduced hours rather than seeing people being laid off. These and other measures won’t prevent a downturn but will help limit the damage.

Finally, we should replace the desultory tax cuts vs. spending increase debate with another choice: tax cuts or debt reduction. Indeed, we need to strengthen our tax base (after the reckless erosion over the last few years under Fine Gael governments) with incremental but persistent increases in taxation starting with the remaining tax breaks that disproportionately favour higher income groups, taxation on property (including unproductive financial property) and passive income (e.g. inheritance and gifts tax).

The last thing we need is scare-mongering about the levels of our debt. Progressives should lead this debate as I outlined in this post. We need a clear analysis and an honest conversation.

We didn’t have that prior to the crash. We didn’t have that during the recession. If we don’t have that now, why should we expect the future to be any different than the past?

Michael Taft is a researcher for SIPTU and author of the political economy blog, Notes on the Front. His column appears here every Tuesday

Again a very interesting article.

One thing I feel is missing is the actual debt in € rather than as a percentage of GDP/GNI*. The improvement in that ratio between 2013 and today isn’t a change in the debt – we’re not paying it off – it is an improved economy.

Between 2000 and 2007 the National Debt was fairly level at ~€38bn.

Between 2008 and 2014 it jumped to €174;

It has stayed level at about ~€185 since 2015.

do you know what we’re paying per annum to service that, cian?

Yes. just over €6bn last year.

NTMA has the full figures: http://www.ntma.ie/business-areas/funding-and-debt-management/debt-service/

joder

12% of exchequer’s tax revenue on interest

and from €1.5bn p.a. before the crash

thanks, cian

True – if you look at the best year *every*.

But if you look down the bottom – in 1997 we “only” had €40bn debt, but the repayments were ~€3bn which was 17% of exchequer’s tax revenue on interest.

yes but when you consider that a lot of recent borrowing went on day-to-day spending rather than investment in infrastructure, it’s still a damning stat

Where do you think the €40bn debt came from that we still had in the 1990s?

It was Charlie Haughey’s government borrowing for day-to-day spending (and – whisper it – buying elections).

http://www.theirishstory.com/2011/01/25/life-and-debt-%E2%80%93-a-short-history-of-public-spending-borrowing-and-debt-in-independent-ireland/#.WuhN9lKpUdU

Cian – that’s correct. The nominal debt level is not falling, merely shrinking in comparison to a rising GDP/GNI*. However, it is unusual for countries to actually reduce their nominal debt. Rather, they ‘control’ it in relation to national output. In Ireland, debt-to-GNP ratio topped out at 117% in 1987. It fell to 82% by 1995 even though the national debt rose from €30 billion to €38 billion. In Germany, the debt-to-GDP ratio fell from 80 to 70 percent, even though the nominal debt rose marginally. Debt is about a relationship though where it is economically prudent, a long-term marginal fall in the absolute level of debt could be entertained. However, this assumes a long-term period of steady growth. And economic cycles are not so kind.

I would love to know the 200 billion of distressed Irish property sold to vulture funds

Where has that money gone?

It certainly was not set off the debt

Did it go to fund more reckless government spending?

Did it go to public sector pay, bonuses, golden hand shakes, pensions,?

Did it go towards the compensation paid out for the incompetence of the HSE and the court cases due to medical incompetence?

Explain that to a ignoramus like me

No mention of increased expenditure for the “benchmarked” public sector which was (and still is) a massive reason why government spending is so high. And despite the booming economy we are still borrowing to pay our bills.

What percentage of government expenditure actually goes to the public sector?

And what (according to you) is the correct percentage?

The percentage of govt expenditure on the PS changes every year, ie when the tax take is large the percentage will be lower than when the there is mass unemployment and emigration. The % is not the key, the AMOUNT is. Which brings me to the point – PS unions should not be let abuse the public purse threatening strikes and commissioning bullsh*t benchmarks to increase their own pay, which has added massively to our soverign debt.

Example of said bullsh*t benchmark from May 1st 2017:

https://www.irishtimes.com/news/ireland/irish-news/senior-civil-servants-get-60-less-than-private-sector-counterparts-study-1.3073375

How much of government expenditure actually goes to the public sector?

And what (according to you) is the correct amount?