From top: Ajai Chopra (right), then Deputy Director of the International Monetary Fund (IMF) European Department, and an associate on their way to a meeting at the Department of Finance to discuss an EU/IMF emergency loan, November 2010; Michael Taft

Economic historians will write of the period we are just emerging from as the ‘lost decade’. When the crash hit, jobs were lost, incomes fell, and government spending was slashed.

It is only now – 10 years or so after the event – we have made up that last ground. Now we have low levels of unemployment, rising income and warnings that the government is increasing spending too fast.

But as we emerge from out of the shadow of the crash, what does the world around us look like?

Well, if Eurostat is anything to go by, we still lag other high-income EU countries in key living standard categories.

Living standards is notoriously difficult to measure. However, Eurostat makes a stab at it with their ‘actual individual consumption’ indicator.This combines personal consumption (consumer spending) and government spending on behalf of households.

This latter is important. If one just took consumer spending as the measure of living standards, a number of anomalies could arise.

For instance, if an Irish household spends €150 per week on childcare while a German household spends only €50, a consumer spending-only measurement would suggest the Irish household had a higher ‘living standard’.

However, under the actual individual consumption (AIC) measurement, the amount of state subsidy on childcare which the household ‘consumes’ is also factored in.

That makes it a superior measurement, especially as it factors in prices for international comparison purposes.

Under these living standard measurements – AIC and consumer spending – how do we fare in 2018?

Factoring in inflation we find:

Per capita consumer spending is still 2.1 percent below the peak in 2008

Per capita AIC is still 3.1 percent below the peak in 2009

Hopefully, this year will see us surpassing pre-crash peaks.

Except just as we are emerging from a lost decade we have warnings of over-heating in the economy.

Question: how could we get to a situation where, after a decade, all we do is return to the point at which we started and, yet, we’re in danger of over-heating?

Some might say that our previous peak was unsustainable. Without getting into that historical argument, this is hardly the explanation today.

Even if we concede the argument that consumer spending and AIC (which includes government spending on behalf of households) was unsustainable in 2008, that argument shouldn’t apply today.

Both consumer spending and AIC are significantly below 2008 levels as a percentage of GNI*; yet now we are being warned that we are at capacity (just like a decade ago).

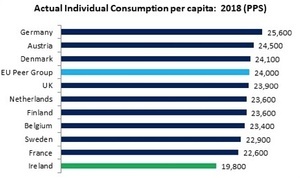

So at this point of full capacity, how does Ireland fare compared to other high-income EU countries, our peer group?

We are far below our peer group average in this living standard measurement. We would have to increase consumer and government spending on households by over 20 percent to reach the average.

When we disentangle consumer spending and government spending on households we find the gap remains somewhat the same.

Both consumer spending and government spending on households are well below our peer-group average, with Ireland coming in at the bottom of the table in both.

Consumer spending would have to increase by 16 percent and government spending on households would have to increase by 40 percent just to reach the average.

So after a lost decade, when we have only returned to pre-crash levels, when our living standards are still well below other high-income EU countries, we have hit a capacity wall suggests the problem is deeper than just fiscal policy (though that is a contributor). It suggests that there is a structural problem.

Now consider the impact of even a ‘managed Brexit’ (?) never mind a no-deal Brexit. We would not only stall, we could start falling backwards.

After a lost decade, we may still be lost.

Michael Taft is a researcher for SIPTU and author of the political economy blog, Notes on the Front. His column appears here every Tuesday.

I’m still waiting for him to tell us why we are at capacity despite some indicators showing us we’re short of our 2008 peaks. Where’s the rest of the article? What’s this “structural problem” he mentions and then says nothing more about?

This. It feels like the 2nd half of this article is missing!

Joe – Hard to know if we have hit capacity since conventional measurements look like output gap suffer from the same issues as our GDP. Some data suggests structural problems (depending on the answer to the capacity question) but this will require more analysis. I suspect it can be found in the under-performing indigenous and non-financial sectors.

Quick question Michael. Every article you have us compared to the high-income EU countries – and we lag far below them most of the time.

However we used to be in the PIIGS. What happened that we’re now being compared to the richer countries? And how do we compare the the other countries.

Past vs present…not really a difficult concept

Cian – the Pigs comparison referred to bailout countries or those with high debt/low growth countries. Nothing else was comparable between Ireland and others (especially with our modern export sector). Neri uses similar comparators (‘advanced European economies ‘). From memory I think Ireland is below the EU average. When measuring euros or PPPs it doesn’t tell us much to compare ourselves with Mediterranean or Eastern European countries as these are much poorer.

I heard my first ” Bulgaria is the place to invest ” since the crash the other day.

Oh we’re back alright.

Another crash not far off so

keep hearing that when I visit companies in Ireland

they are very aware and are planning for the next crash that is “just around the corner” or “in the next 4-5 years”

Very concerning how many MD’s mention this. There is little positivity past 4 years.

Tight times are a-coming. Let’s brace ourselves. We can’t eat macroeconomic statistics.

Very selective with the stats this week, the plain truth is Ireland Inc is currently 200 billion in debt vs 50B in 2008. It’s why the govt can no longer simply throw money at public sector unions (a major cause of our debt) & so we’ve had strikes in the HSE.

From today’s IT:

http://www.irishtimes.com/business/financial-services/ireland-s-200bn-debt-burden-how-did-we-get-here-1.3943085?

why arent we paying down this debt with the extra cash to avoid interest in the future if interest rates allow us to?

What extra cash? The state still borrows money every year specifically to pay for the pay & pensions of the public sector.

We’re breaking even since last year. This year there should be some surplus.

Counties rarely pay off debt. They roll it over.

Over time inflation will deal with it.

Ireland had 40bn debt from the 80s (when GDP was about 40bb)… and rolled.it over and over until 2006. It was still 40bn but our GDP had grown to almost 200bn.

During this time the multi nationals arrived. We do not have another economic Hail Mary in the works, instead we have Brexit looming.

And that’s it in a nutshell. There’s also the little issue of trust. Average Eddie (who I consider myself to be) still doesn’t trust the state not to fook things up again. I’m – by better off European standards – very conservative in my spending, I doubt i’m alone. We have long memories. Combine this with the states simple inability (because of the phenomenal rise in our national debt) to spend like other “better off” neighbours and there’s no confusion about why living standards here might be considered as lagging behind.

Sure everyone has a new SUV

You look like a dope now if you don’t have one

Better get in line for a PCP agreement or you wont be cool

It’s a “no brainer” as the No Brainers would say, loud enough so the whole restaurant can hear them proudly announce.

Cian – the Pigs comparison referred to bailout countries or those with high debt/low growth countries. Nothing else was comparable between Ireland and others (especially with our modern export sector). Neri uses similar comparators (‘advanced European economies ‘). From memory I think Ireland is below the EU average. When measuring euros or PPPs it doesn’t tell us much to compare ourselves with Mediterranean or Eastern European countries as these are much poorer.