Michael Taft (above) writes:

Today, just six working days into the New Year, the average remuneration for CEO’s in the top 26 Irish companies (which represent 95 percent of the market value of the Irish Stock Exchange), has already exceeded the average yearly pay for a full-time employee.

The rest of the year is cream.

ICTU has release their latest survey of CEO compensation. They found that in the top 26 Irish companies CEO pay – basic pay, bonuses, long-term investment plans, benefits-in-kind and pensions – now averages €2.3 million. This compares to annual compensation for a full-time employee of €53,800 (including employers’ social insurance and other in-work benefits).

Starting at the top we find the CEOs in CRH, Kerry Group, DCC, Tullow Oil, Paddy Powers and Ryanair all had compensation packages in excess of €3 million.

In 20 of the 26 companies, CEO pay exceeded €1 million.

Not only is the level of CEO remuneration high, the rate of growth has also been high. Between 2009 and 2015 – the years when we were all supposed to be tightening our belts – the average increase in CEO remuneration was 75 percent, or €890,000.

Average employee compensation for full-time employees increased by 1.6 percent, or approximately €850.

In 2017, this upward trend continued though at a slightly slower pace. Average CEO pay increased by 6 percent. This compares to an increase for full-time employees of 1.7 percent.

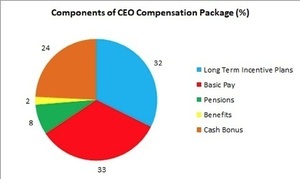

CEO compensation is made up of a number of components:

Basic pay makes 33 percent of total compensation. Long Term Incentive Plans (generally share options) make up another third with bonuses making up a quarter.

Some may argue that CEOs earn their level of remuneration. However, there is no consensus among scholars regarding a link between CEO pay and firm performance. Indeed, there are links between high pay and negative economic and enterprise impacts.

Chris Dillow’s post here refers to a number of studies that show high pay can lead to lower productivity, perverse incentives, and a disproportionate focus on short-term indicators at the expense of long-term outcomes such as investment.

Further, we should remember that CEO pay is not set by the ‘market’ but rather by remuneration committees; in other words, the CEO’s peer group. The purpose of these committees is to provide a robust criteria and company comparisons in order to set CEO pay.

But as TASC’s report, Mapping the Golden Circle, points out, there can be an incestuous relationship between, CEOs, Board Directors and members of remuneration committees.

The latter sit on the boards of companies and board directors can be CEOs or senior executives of other companies:

‘ . . . executive compensation in large publicly traded firms often is excessive because of the feeble incentives of boards of directors to police compensation … Directors are often CEOs of other companies and naturally think that CEOs should be well paid. And often they are picked by the CEO.’

To put it another way, what would be the reaction if we proposed that workers set the wage of other workers in comparable firms by committee?

If high CEO pay has negative economic and firm consequences, along with offending our more egalitarian instincts, what can be done? ICTU has a number of suggestions:

Require companies to set objective criteria for CEO pay including factors such as employee welfare and environmental protection as well as financial performance

Expand the remit of the Low Pay Commission to monitor the relationship between highest and lowest pay

Report on the use of temporary agency workers and sole traders (which in many cases are used to drive down payroll expenses)

Make shareholders’ decisions on executive pay binding rather than advisory (yes, the ‘owners’ of the company do not have an automatic right to collectively set pay – so much for ‘ownership’)

A higher tax on very high incomes (e.g. in excess of €1 million).

However, if high executive pay is part of a larger picture, we need broader economic and social strategies to address the problem of the widening gap. There isn’t the space to go into that here but as a start I would propose the extension and deepening of collective bargaining.

As the OECD pointed out – and discussed here – the top 1 percent have a lower share of income in economics where more workers are covered by collective bargaining.

This makes sense: collective bargaining puts upward pressure on low and average incomes and, so, puts downward pressure on higher incomes – whether in the firm or the economy.

There is no magic bullet in all this.

ICTU continues to do the debate a service in providing annual information on CEO pay. Hopefully, this will provoke greater public, political and academic interest in the subject. Excessive gaps in income and high levels of inequality are socially corrosive and economically inefficient.

If we’re not careful, every day in the future will be a day for fat cats.

Michael Taft is a researcher for SIPTU and author of the political economy blog, Notes on the Front.

A couple of points:

1. “high CEO pay has negative economic and firm consequences” – you haven’t provided any evidence for this. You have linked to a study that claims there is no relationship between remuneration and performance. That’s something entirely different. Don’t conflate the two.

2. Besides “egalitarian instincts” why does it matter whether CEO’s earn big remuneration packages? Isn’t this an issue for the shareholders more so than anyone else? If big remuneration packages are bad for companies (you provided no evidence for this) then the shareholders would act accordingly.

3. your point on the “Golden Circle” – Dublin is a small city, it’s not surprising that directors and CEOs across all these companies have business relationships. You keep batting this report but it does nothing for your argument. It’s not incestuous, it’s a small business community. Also, your report refers largely to the pre-GFC industrial order and excludes private companies and the new burgeoning tech and financial sectors.

“Besides “egalitarian instincts” why does it matter whether CEO’s earn big remuneration packages? Isn’t this an issue for the shareholders more so than anyone else?”

+1

If shareholders are happy to pay their CEOs a big salary, that’s their business; just if SIPTU members want to give their President a six-figure salary, that’s their business.

This idea of “Require companies to set objective criteria for CEO pay including factors such as employee welfare and environmental protection…” sounds incredibly vague and difficult to enforce.

Jonickal – thanks for that. You raise a number of points.

First, studies linked in the Chris Dillow post (which I link to) provide access to studies that show the downside of high CEO pay (he is writing in the UK context where, like the US, CEO pay is really off the charts).

Second, pay, income and social inequality matters. Shareholders do not have legal powers to amend CEO pay (in many cases, they are advisory only), CEO pay and all all pay and employment contracts within a firm should be an issue for all stakeholders; in particular, the largest stakeholders – employees.

Third, large or small, the make-up of remuneration committees is determined by those who benefit the most. There are other models – including employee representatives and industry experts not associated with the company or companies in relationship. I refer to the TASC paper since it is the only detailed assessment of the relationships we have. You are right – it would be helpful to have an update but I have not seen any.

Michael

The CRH CEO had total compensation of €8.7m in 2017. CRH employs 87,000 people. So thats c.€100 per employee. If you wiped the compensation package down to a few hundred grand, and redirected all of these savings to employees, they’d get €90 or 0.2% increase in pay. Its unclear how this would make much of an actual difference to broader society other than by making some of the CEO stats look better/lower. CEO pay packages are generally over the top relative to what should be required to employ these people, and yet they don’t make a huge difference to the broader economic situation either. They’re the distraction, not the problem. CEO’s are part of the labour side of the economy just as much as the lowly production line worker. If (*if*) there really is a maturing element to our long term business investment cycle (secular stagnation etc), then its changes to tax treatment of capital gains and dividend income that are likely to have a much greater impact on inequality (although the potential for policy mistakes here are enormous)

“A higher tax on very high incomes (e.g. in excess of €1 million).”

Ireland already has the most progressive income tax in the OECD, with (AFAIR) the top 5% of earners contributing something like 40% of the total income tax take – how much more can they be reasonably expected to pay?

France already introduced a similar tax – they quickly scrapped it when all of the millionaires moved to Belgium; I can’t see any reason to suppose a different outcome if it was introduced here.

Taft is just another loser trying to drag motivated hard workers down to his level of mundanity and failure.

Are you enjoying those Ayn Rand books?

Splutter.. hahaha.. aaaahh mercy.

Hat tip, nod and wink to you, take a bow or just carry on regardless…

:-J

+1

Is “Ganbia” in the chart some kind of famine-related charity?

heehee

Meh, just get a job as a CEO of a top company then.

“Basic pay makes 33 percent of total compensation. Long Term Incentive Plans (generally share options) make up another third with bonuses making up a quarter”

would regular employees accept that pay structure and would unions support it?

CRH have 85k employees worldwide, comparing the CEO’s pay to any average of their employees is nonsensical