From top: Morning commuters in Dublin city; Michael Taft

From top: Morning commuters in Dublin city; Michael Taft

The EU Commission makes an interesting observation on in-work poverty:

‘ . . . in-work poverty is certainly becoming more prominent in policy discourse and action . . . However, the concept of “in-work poverty” is often not used as such, and discourse focuses on alleviating poverty in general.’

That’s not surprising. It is difficult for many policy-makers and commentators to discuss in-work poverty for the simple reason that employment is portrayed as way out of poverty.

When it is shown not to be for significant sections of the population, the pathway argument collapses.

Similarly, in Ireland: ‘in-work poverty’ is not generally discussed (though there has been considerable discussion of the Living Wage). Hopefully, the Nevin Economic Research Institute’s latest findings will contribute to changing that.

There are a number of ways to measure in-work poverty. The main statistical measurement is relative, or ‘at-risk’, poverty. This measures the percentage of workers whose income is 60 percent below the national median income.

The national median income is the midway point (50 percent above, 50 percent below) for all people in society, not just those in work. On this measurement Ireland looks good when compared with our EU peer group.

However, when comparing median incomes we’re not on the same pitch. This means that in Ireland, work income would have to be significantly lower than the other countries to be classified as ‘at-risk of poverty’, or 60 percent of median incomes.

That’s because Irish median income is significantly poorer.

That is why when using relative measures we have to look at not only the rate but the denominator (median income) as well. This is not to dismiss relative measures; only that we need to be aware of what we are measuring.

There are other measurements – soft measurements. These are not statistically based like ‘at-risk of in-work poverty’. These measurements, collected by the CSO and Eurostat, are based on asking people about their living standard.

This is what NERI presented last week, using two measurements: deprivation and inability to afford an unexpected expense.

(a) Deprivation

The CSO defines deprivation as experiencing two or more deprivation experiences ranging from an inability to keep house warm, affording two pair of strong shoes or a warm waterproof coat, to affording a substantial meal every two days, or a morning/evening out in the last fortnight.

NERI’s findings are concerning:

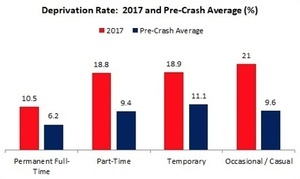

Over 10 percent of permanent full-time employees are officially classified as living in deprivation conditions while part-time, temporary (fixed-term) and occasional employees come in at approximately 20 percent. These are dismal numbers.

Deprivation rates are still well above pre-crash averages (the average for 2002 – 2008) despite significant increases in national income. They have, at least, declined from recession highs. For instance, deprivation among full-time employees was 16.7 percent in 2014.

However, between 2016 and 2017, the rate barely fell by 0.2 percentage points. In fact, in 2017 the deprivation rate for two-income households actually rose over the previous year – from 9.2 percent to 10.7 percent.

(b) Inability to Afford an Unexpected Expense

Nearly 30 percent of permanent full-time employees are unable to afford an unexpected expense. This rises to nearly 40 percent for part-time employee and even higher for temporary employees.

Occasional and casual workers fare the worst with over half unable to afford an unexpected expense. The numbers are significantly higher than pre-crash numbers.

Unfortunately, we don’t have European comparisons for either deprivation or unexpected expenses for those in work. The following looks at deprivation rates among all 18-65 year olds.

This, at least, captures the working age population. The unexpected expenses data relates to those above the relative poverty threshold so, again, this is likely to be largely made up of people in work.

While indicative, the data shows Ireland topping the deprivation and unexpected expenses tables.

There is no magic bullet that can bring down rates of deprivation and precarious living conditions. One thinks of increasing the minimum wage – and there’s nothing wrong with that.

However, we shouldn’t assume that all the households affected are on the minimum wage.

Much depends on circumstances. If you’re paying €1,500 a month in rent, a few extra Euros in the pocket isn’t going to make much of a difference.

However, cutting rent by a couple of hundreds of Euros would be a significant gain in living standards.

Similarly, with families facing childcare costs, school costs, etc. – reducing these costs would go much further than a wage increase.

Getting a few extra hours of work would have significant benefit for those on low-hour precarious contracts.

Addressing these issues requires a number of inter-locking strategies:

Reduction in living costs

Collective bargaining

Reduction in precarious work contracts

Stronger statutory or sectoral wage floors

If we truly want employment to be a route to prosperity, if we want to reduce poverty in the economy, we need to take in-work poverty seriously. The first step is to start actually naming it so we can start debating it. These are the first steps to eventually abolishing it.

Michael Taft is a researcher for SIPTU and author of the political economy blog, Notes on the Front. His column appears here every Tuesday.

People on minimum wage or above don’t pay 1,500 per month in rent, they would qualify for HAP. If they qualify the landlord is legally obliged to accept it.

Only way is to increase wages, we need to get out of this low wage mindset. People should be rewarded for working.

No landlord needs 1500 from a tenant. It is greed pure and simple . Rent everywhere should be capped at 1200 at the absolute maximum . In fairness anything over 900, the landlord is Boomer “I’m barely keeping my head above water myself” scum. But that’s never going to happen when every single politician in this country has a second property that they are renting out for maximum profit. If tenants had an extra hundred quid a week to spend elsewhere (or god forbid have the chance to actually save money ) then other businesses can maybe make more money and pay their staff more. At the moment everyone’s money is spent on the already bailed out scumbag FIRE industries. Only mortgage holders have the extra cash to spend elsewhere. My house in the suburbs costs me a thousand euro a month less than what some renters pay. How is that fair?

I assume your talking about €1200 per tenant, so for a 2 bed house that’s €2400

Leaving aside the monthly repayments on a 2 bed house, leaving aside all the angst, gnashing of teeth, sense of entitlement something for nothing utopian ideal of most non-business people on Broadsheet

Taking that rental income of €29k per annum, taking off expenses, repairs, insurance, tenancy board fees, utilities, allowable mortgage interest, non payment of rent, the average landlord will be left with maybe €17k rental profit margin. They pay 40% tax on that so that leaves €10k after tax.Or €833 per month – yaay.

But

Now you’ll note that only allowable mortgage interest is expensible. So going in to the rental agreement, based on a rent of €29k per annum. In order to walk away with the princely sum of €833 per month – off to the yacht dealership – The rent will need to cover the mortgage. Hate to tell you but €2400 a month doesn’t cover too many historic mortgages in Dublin – in fact it’s less than the average Dublin monthly mortgage repayment last year

SO. ignoring your comments about scum etc – just makes you look an idiot – your idea to cap rents is poor but there may be a case to come up with some way of capping profit.

You should come out of retirement more often, wearnicehats, you are a pillar of sense.

Your comment implies an entitlement to profit on rental income after tax.

This ignores the value of the asset the landlord has (in most cases – I haven’t seen numbers on how many rental properties in Dublin are still in negative equity).

negative equity only counts if the landlord has a mortgage on the property he is renting out. what if he own it? landlord do own properties outright you know? , not that any of them would admit it. 30k profit a year before tax every year for doing essentially nothing? If you own a second house , you shouldn’t be gouging renters 2400 a month for a two bed house.

What do you mean exactly Col? Are you suggesting that people shouldn’t have the right to benefit at all from their asset?

Now negative equity. People love that expression. For every chancer landlord there’s a reluctant landlord ie one who was sold an idea is now stuck with something that is uneconomic to offload. These are, ironically, the kind of people that had the likes of postmanpat’s schadenfreude jumping out of its skin back in the day.

Anyway, it was estimated that about 16,000 investment mortgages were in negative equity at the end of 2018 but I would say that is on the low side given property price fluctuations in 2019.

And just because your property is worth less than your mortgage doesn’t mean that you’re not in negative equity. You know how I love meaningless stats. There could be thousands more cases where the property is worth maybe 1% less than the mortgage but the owner has so much historic debt that their overall liability is still swamping them. Don’t forget that those people who got burned in the boom times had to borrow a lot of money to get their deposits. They also had to pay, in most cases 9% stamp duty on top so given the boom prices some people had to find an additional (on top of deposit) maybe €60-70k just to give to the government. ie they borrowed money to be allowed to borrow money. So the point is that just because you’re not losing out doesn’t mean you’re not losing out, if you know what I mean

And the figures don’t allow for the tax payable when you sell your home. Or hand it down to your children. I personally would vote for any party who allowed people to deduct their stamp duty from their Capital Gains Tax liability. But, of course, the one glimmer of good news for most is that, when they sell, very few of them will actually have to pay any Capital Gains tax because most boom properties will go for a sales price way below the purchase price

I know one family, for instance, who live with relatives and rent their own home out so that they can afford to service their debt without having to sell the house. They are not living the dream. They are not “scum”

Glad to see that postmanpat is at least not being a little more selective in his bile. HE might want to look at just how many landlords fit in to this bracket. And don’t use the word gougers. Try to be polite, people are more likely to listen to you

And some old queen – maybe this covers some of your post

wearnicehats , you mentioned “sense of entitlement” and then spoke about the entitlement to make profit on rental income after tax and expenses.

“Are you suggesting that people shouldn’t have the right to benefit at all from their asset?”

No.

Yes that is the problem- people who are landlords have many circumstances- like the one you describe. But, on the other extreme there are plenty of landlords who not have any mortgages at all- I know one in particular with FOUR apartments now paid outright and- has retired at 50. Oh and he sings the poor mouth too of course.

But, the one thing everyone should agree on is that that tax on rent is way to high. I don’t see much renter vitriol towards the government when in fact, they cream 40%+ of ALL rent paid.

* who have no mortgages at all.

“But, the one thing everyone should agree on is that that tax on rent is way to high. I don’t see much renter vitriol towards the government when in fact, they cream 40%+ of ALL rent paid.”

That’s because rental prices probably wouldn’t come down much, due to supply & demand, so renters wouldn’t benefit. They’d be more likely to look for rental relief.

Fair point wearnicehats but if current rent is not covering some people’s mortgages then they should sell up because nobody is forcing them to keep them and nobody forced them to take on unsustainable mortgages in the first place.

I find it hard to have sympathy for landlords in the current market, accidental or otherwise- they have a choice which is a hell of a lot more than renters do.

Glad to see that postmanpat is at least now* being a little more selective in his bile

Salaries in Ireland are shockingly low – especially for a generally well-educated and computer literate workforce. And Dublin salaries should be weighted.

Two things:

1. I totally agree with the conclusions and I think the focus should be on reducing the costs of living.

2. I have a bit of a problem with the range of the “Deprivation” questions. There is a vast difference between someone not being able to afford a warm waterproof coat and not being able to replace worn-out furniture – but both are deemed ‘deprived’.

Changes in % of individuals suffering deprivation from 2012 to 2017

Without heating at some stage in the last year 13.0% to 8.1%

Unable to afford

…a warm waterproof coat 3.7% to 1.6%

…a meal with meat, chicken or fish every second day 4.0% to 1.7%

…two pairs of strong shoes 4.9% to 3.3%

…to buy presents for family or friends at least once a year 5.9% to 4.2%

…to keep the home adequately warm 8.5% to 4.4%

…a roast once a week 7.7% to 5.3%

…new (not second-hand) clothes 10.4% to 8.0%

…a morning, afternoon or evening out in the last fortnight 23.4% to 13.2%

…to have family or friends for a drink or meal once a month 16.2% to 13.9%

…to replace any worn out furniture 24.5% to 20.4%

https://www.cso.ie/en/releasesandpublications/ep/p-silc/surveyonincomeandlivingconditionssilc2017/povertyanddeprivation/

The biggest single factor for the working poor, at least those renting, is accommodation costs. Wages have remained stagnant or as near as, while rents keep rising. In the last budget they gave a tax break to landlords but not to tenants- says it all really. But what was really sinister was that RTÉ 9 O’clock news never even mentioned it- they deliberately ignored it.

Given that so much of that rent goes to government in tax, they could easily fix it if they wanted to- but they don’t- not even FF would be that callous.

The huge cost of living is the elephant in the room……..

Useless planning regulations that force workers to expensive commutes…

The outrageous legal gravy train that everyone pays for anytime they buy anything (even a cup of hot coffee). The compo culture lawyer bonanza is paid for by every taxpayer.

Incompetent, unaccountable and unfirable public servants so useless that despite paying them with our taxes they are unable to provide simple services like clean water or waste disposal. You pay extra for that. You also pay for private health insurance due to the incompetence of those who “organize” the public health system which already costs you over 13 billion annually.

etc, etc.

There is no point on comparing pre-crash to now, it was a lie built on credit that wasn’t and couldn’t be repaid