From top: Early morning commuters on a Dublin Bus last January; Michael Taft

There is a growing interest in reducing the working week – usually expressed as a four-day week. Numerous ad hoc examples of private and public sector companies and agencies appear in the media while, here in Ireland, Forsa recently held a conference dedicated to reducing the working week.

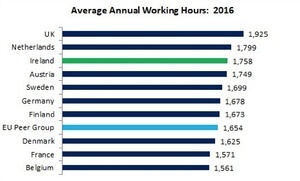

The arguments for a shorter working week range from greater work/life balance, productivity, stress reduction, preparing for the impact of automation, etc. As part of that debate below is some information on how many hours per year people work in Ireland in comparison with our EU peer group (other high-income economies).

This data focuses on full-time employees but it should be noted that full-time is defined as approximately 30 hours by the CSO with possible different definitions in other countries. Further, this looks at the private sector as this is where the introduction of a shorter working week on the same rate of pay will be the most challenging.

The Private Sector Economy

Irish employees work more hours than most other peer group countries. The UK and the Netherlands report higher annual working hours. The Netherlands is an interesting case. It has the highest level of part-time workers with 50 percent of all employees working part-time compared to an average of less than 25 percent in other countries.

Annual working hours can be reduced in many ways – not just a though a shorter working week. For instance, public holidays, statutory annual holidays and additional holiday hours resulting from collective agreements in the workplace can reduce annual hours worked.

In total, Irish employees work the equivalent of 2.7 weeks more than our peer-group average, assuming a basic 39-hour working week (the UK is not included in our EU peer group for obvious reasons; Eurostat is already removing the UK from EU averages). We don’t work the most, but we work more than most in our peer group.

Working Hours by Sector

The following looks at sectoral breakdowns. Let’s start with the high working-hour sectors.

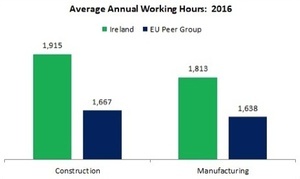

Irish construction employees work more hours than any other sector, and 15 percent more than our peer group average – 248 hours annually, or the equivalent of 6.4 weeks more per year. A possible contributor to this high level of working could be the emerging labour shortage in the sector.

Irish manufacturing employees work 11 percent more than our peer group – 175 hours annually, or the equivalent of 4.5 weeks more per year.

Turning to medium-high working-hour sectors we find the following.

Irish transport employees work 8 percent more than our peer group – 132 hours annually, or the equivalent of 3.4 weeks more per year.

Irish wholesale/retail employees work 6 percent more than our peer group – 106 hours annually, or the equivalent of 2.7 weeks more per year.

Irish communication and information employees work 2 percent more than our peer group – 37 hours annually, or the equivalent of nearly one week per year.

Irish financial services employees work 5 percent more than our peer group – 76 hours annually, or the equivalent of nearly two weeks per year.

Finally, let’s look at relatively low working-hour sectors.

Irish professional and technical employees work 1 percent more than our peer group – 11 hours annually, or the equivalent of less than two days per year.

Irish administrative service employees work marginally less than our peer group – less than half-a-day per year.

Irish hospitality employees work 3 percent less than our peer group – 53 hours less, or the equivalent of 1.4 weeks per year.

It should be noted that the hospitality sector is likely to have high levels of precariousness. The problem here may be that full-time employees don’t get enough work.

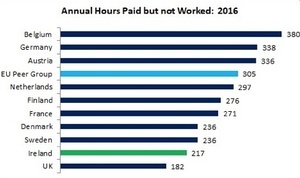

It’s bad enough that we are over-worked compared to our peer group. But we also get fewer paid days off.

Annually, Irish workers get 88 fewer hours paid without working than our peer group average. That’s the equivalent of 2.3 weeks fewer paid public holidays, annual holiday leave, etc.

Some might say this is the price we must pay to have a strong economy. However, other economies with far fewer working days and more paid days off have just as strong economies.

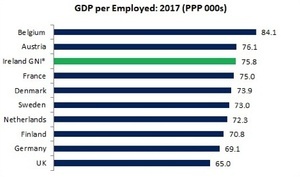

Belgium, which has the lowest annual hours worked and the highest number of paid days off, has the highest GDP per person employed (factoring in living costs). On the other hand, the UK has the highest working hours and the fewest paid days off.

Yet they are at the bottom. Ireland, while ranking third, is clumped together with a number of other countries which have fewer working hours and more paid days off.

In short, working more doesn’t guarantee higher output.

Hopefully the debate over the future of the working week will gather pace.

But one thing is for sure. Irish workers are already over-worked. What we need is fewer working hours and more paid time off.

Now.

Michael Taft is a researcher for SIPTU and author of the political economy blog, Notes on the Front. His column appears here every Thursday.

Top pic: Rollingnews