The Government’s concern is with how any further rise in property repossessions may add to the problem of homelessness. In this regard, tenants in the buy-to-let sector, who are less well protected, are likely to be worst affected. The Department of the Environment and the Department of Finance are considering “duty of care” legislation, which would prohibit banks and lenders evicting a tenant who had no alternative accommodation.

Quite whether this can be achieved remains to be seen, given the potential difficulties such legislation presents – not least on constitutional grounds. At present sitting tenants in buy-to-let properties may well be the last to hear about legal moves taken by banks and lenders to secure repossession orders, as the issue is contested between lenders and landlords, and sitting tenants are mere bystanders.

A welcome first step to protect tenants in buy-to-let housing (Irish Times editorial)

Constitutional grounds?

Potential difficulties with such legislation?

We asked Legal Coffee Drinker what’s it all about.

Broadsheet: “Legal Coffee Drinker, what’s it all about?

Legal Coffee Drinker: “Sitting tenants in buy to let properties secured by a mortgage are at risk of eviction if the lender has not consented to their tenancy. Most mortgages contain a clause prohibiting the borrower from entering into leases or tenancies without the consent of the lender. Leases and tenancies so entered into are valid against the borrower landlord but void against the lender. This usually only presents a problem if the borrower gets into arrears and the lender applies to the court for a possession order, to get rid of the tenant. Such order will generally be granted, unless it can be shown that the lender has consented to the tenancy.”

Broadsheet: “And what if the lender has consented to the tenancy?”

LCD [unwraps Nespresso ‘Arpegio’ capsule]: “If the lender has consented to the tenancy, or if the mortgage permits letting without the consent of the lender, then the lender is bound by the tenancy and cannot be granted possession of the property until the tenancy ends.”

Broadsheet: “So any prospective tenant of buy to let property should ask if there is a mortgage on the property and if so whether the lender is consenting to the letting?”

LCD: “They can ask, but in a high rental market the landlord may not want to rent to tenants who are asking difficult questions.”

Broadsheet: “If a tenant is dispossessed in this way, can they even get back their deposit?”

LCD: [pause] “The tenant has a right to get back their deposit from the landlord, but not from the landlord’s lender. If the landlord does not have funds, then the tenant will not recover their deposit.”

Broadsheet: “So basically a huge category of tenants is in a very insecure position.”

LCD: “Absolutely. There is a stark division between tenants whose landlords have a mortgage, and those who have not.”

Broadsheet: “Can this be changed by legislation, to give the tenant more protection?”

LCD: “Easily. One very simple step would be to legally require landlords, when offering a tenancy for letting, to provide evidence of lender consent to lettings of the type offered. Alternatively, the law could be changed to make all lenders of buy to let property bound by lettings granted by the borrowers whether they had consented to them or not.”

Broadsheet: “Would this be a breach of the property rights of the lender?”

LCD [Drains coffee]: “Not if the lender was granted the rights of a landlord under the Residential Tenancies Act. Such rights, which include not only the right to have the rent increased to market rent in the case of below-market rent lettings (Part II of the Residential Tenancies Act) but also the right to determine the tenancy on notice in the event that the property is being advertised for sale (Section 34 of the Act), provide perfectly adequate protection for buy to let lenders while at the same time ensuring that the tenants retain the same level of protection as they would have if the property was not buy-to-let.”

Broadsheet: “So there’s no constitutional property rights bar to a change in the law in this area as the Irish Times suggests?”

LCD: “No. In fact, far it could be argued that there’s a constitutional requirement to implement such change to protect the property rights of tenants.”

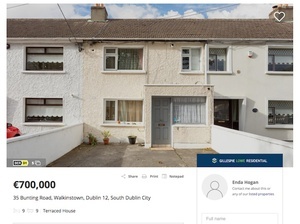

A Welcome First Step For Buy To Let Tenants (Irish Times)