This morning.

Dun Laoghaire, Co Dublin

Piajade notes:

Duffys are promising a lot….

This morning.

Unspecified location, Dublin.

Free lanes!

Sam Boal

Last night.

Herbert Park, Dublin 4

Thanks Luke Brennan

Devon grandmother Rozamund Perrin and underwear posted to her with an angry note.

If you buy a cottage in Devon

don’t hang on your washing line seven

Pairs of frilly pants

Or you’ll receive rants

Of the kind that you won’t hear in Heaven.

John Moynes

Pics: Kent Express & Echo

From top: Enda Kenny with newly appointed High Court judge Una Ni Raifeartaigh SC at the Aras on Tuesday; Dan Boyle

‘Personal magnetism’, a high ‘sex drive’ and an ‘ability to cast spells’.

Everything we need in a hip, happening taoiseach.

Dan Boyle writes:

The Taoiseach awoke from his hibernation this week to tell us he has his mojo back.

I suspect he was referencing the definitive Muddy Waters‘ version of the song ‘I’ve Got My Mojo Working‘ from 1956. Muddy didn’t write the song, nor did he record the first version, but he made the song his own.

By way of diversion can I say that aside from his distinctive blues guitar and voice, I’ve always loved the name Muddy Waters. It works just as well as a political verb.

Back to the mojo in question, that of the Taoiseach. The dictionary definition gives some indication as to what the Taoiseach has been trying to get across.

It explains mojo as –

A magic charm, hex or spell; associated with the African/American religious practice of voodoo. Supernatural skill or luck.(slang) Personal magnetism; charm.(slang) Sex appeal; sex drive.(slang) Illegal drugs.(slang, usually with “wire”) A telecopier; a fax machine.

Quickly moving on from the idea of the Taoiseach being a hex worker, the illegal drugs are probably best avoided, but I would have thought the metaphor of being a fax machine is crying out to be used.

The danger of using cultural slang is that you may end up missing the zeitgeist.

Mojo is more Kerouac than Eminem (and Eminem isn’t exactly the zeitgeist). If it’s hip and happening you want to be then mojo is your man. If it’s happening and hip you’re looking for you’ve kind of missed the bus.

The answers in Enda Kenny’s interview with Pat Kenny have little to do with the interviewer. Neither is the general public the intended audience. This exercise in braggadocia is strictly for the Fine Gael parliamentary party.

Apparently if you make yourself appear big in front of a bear, the bear would be less inclined to challenge you. This is the Taoiseach’s strategy.

There is some indication that it might work. It could also be argued that John Halligan, with his Waterford stand-off, is employing a similar strategy. Being able to appear bear like would further help this strategy.

The Taoiseach has about a dozen years on me. When I think mojo I think back to my lost, much mythologised, youth. That time when I did all night what it now takes me all night to do.

I suspect we may not be thinking about the same thing but I’m fairly sure we are about arriving at the same destination. If we’re not careful Naomi Klein’s next book may be called ‘No Mojo’

Dan Boyle is a former Green Party TD and Senator. Follow Dan on Twitter: @sendboyle

Rollingnews

MORE to follow.

This evening.

On RTÉ’s Six One.

Chairman of Nama Frank Daly was interviewed by Brian Dobson.

At the very end of the interview:

Brian Dobson: “You still say tonight, that the taxpayer got full value?”

Frank Daly: “I say, absolutely, the taxpayer got full value for money. And I say it even more strongly now in a post-Brexit environment. If we were trying to sell that portfolio now – we would not get offers anywhere near £1.32billion).”

Watch back in full here

Alternatively…

Namawinelake writes:

What loss did Nama make on the Project Eagle transaction?

Depends on how you define “loss”!

The Nama projection of its ultimate profit by 2020 is €2.3billion. If it hadn’t sold Project Eagle in 2014, and worked the loads out between 2014-2020, the ultimate profit would be €2.74billion. So, the loss is €440million*.

By selling the loans in 2014, Nama did not generate £1.68billion in projected net cash receipts by 2020 on those loans. Instead, it sold the loans for £1.3billion.

So, the loss is £380m (€444m). This loss arose from two decisions (1) the decision to sell in 2014 rather than manage the loans until 2020 and (2) the decision to sell the loans below Nama’s own valuation.

On the other hand, if you compare the safe value of the loans in 2013 (£1.3billion) versus the Nama valuation of the loans in 2014 (£1.49billion), the loss is £190million (€222m).

Facts

1- Nama has until 2020 to manage its loans so as to maximise their value for the taxpayer. Nama did not have to sell the loans in 2014; it could have managed the loans until 2020, which would have resulted in the loans generating £1.68billion, according to Nama’s own projections.

2- Nama used the proceeds from the sale of Project Eagle to redeem senior bonds which have a zero (technically a minus) interest rate. Nama could have used the proceeds from the Project Eagle sale to invest in its assets, but it didn’t; Nama used the cash to pay down its own debt which cost it nothing.

Report Extracts (which emphasis added).

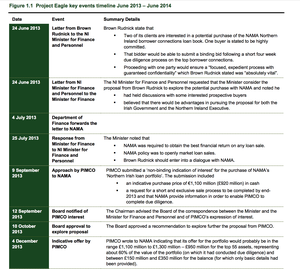

“In a paper submitted to the Board for the December 2013 meeting (reproduced in Appendix C) the Nama executive sought the Board’s approval for the sale of the loans. The paper indicated that the total Nama debt for the loans at the end November 2013 was £1.98 billion – equivalent to 43% of the par debt.”

“Cash flow projections indicated that Nama would realise net receipts totalling £1.68 billion over the period 2014 to 2020 if it worked out the loans through the sale of the underlying assets in line with its formal strategy.”

“The minimum price of £1.3billion set for the sale of the Project Eagle portfolio was significantly less than Nama projected it would realise from working out the loans – an estimated £1.68billion, equivalent to £1.49billion in NPV terms, using Nama’s standard discount rate.”

“The difference between the minimum price and the projected NPV of the workout was up to £190million, depending on the extent to which the adjustment of the 2017 disposal proceeds was valid.”

“As a result, the decision to sell the loans at £1.3billion involved a significant profitable loss of value to the State.”

“Ultimately, the loss incurred when the sale was completed was recognised in Nama’s financial statements for 2014.”

Previously: ‘A Probably Loss Of Value To The State Of Up To €190million’

UPDATE:

Independents 4 Change TD Mick Wallace writes:

“For too long the Minister for Finance and Taoiseach have displayed breathtaking indifference, and at times arrogance, to any form of oversight of NAMA.

The C&AG report deals with just one aspect of NAMA’s operation – if the Government want all the truth in the open, only a truly Independent Commission of Investigation has any chance of exposing just how dysfunctional this organisation has been, and what the cost has been to the people of Ireland.

Until then, the proceeds of the sale of Project Eagle should be frozen, under the ‘Proceeds of Crime Act’ and all NAMA activities should be suspended.“

Previously: Project Eagle And the €3.5billion Haircut

The Comptroller & Auditor General’s report into Nama’s Project Eagle sale and a timeline of the sale, as set out in the report

The Comptroller & Auditor General’s report into Nama’s sale of its Northern Ireland property portfolio, Project Eagle, to Cerberus has been published.

From page 10 of the 158-page report:

The sales of Northern Ireland debtor assets outside Project Eagle involved disposals of 125 properties – mainly in Germany and Great Britain – and represented about one eighth of the carrying value (after impairment) of the Northern Ireland debtor portfolio.

On average, NAMA incurred losses of around 1% on those sales. The corresponding loss rate on Project Eagle was 13%.

From page 11:

In a paper submitted to the Board for the December 2013 meeting (reproduced in Appendix C), the NAMA executive sought the Board’s approval for the sale of the loans.

The paper indicated that the total NAMA debt for the loans at end November 2013 was £1.98 billion – equivalent to 43% of the par debt.

Cash flow projections indicated that NAMA would realise net receipts totalling £1.68 billion over the period 2014 to 2020, if it worked out the loans through the sale of the underlying assets in line with its formal strategy. The paper recommended a minimum price of £1.3 billion be set for a loan sale.

…In June 2013, the NAMA Board endorsed the use of a standard discount rate of 5.5% to evaluate the viability of potential transactions or commercial decisions, including decisions whether to hold or sell an asset.

The examination team applied that standard rate of 5.5% to the projected cash flows in NAMA’s December 2013 paper, and estimated the loans had a NPV of £1.49 billion. This amount represents the probable value to NAMA, as at the end of 2013, of working out the Northern Ireland debtor loans.

As a result, the decision to sell the loans at a minimum price of £1.3 billion involved a significant probable loss of value to the State of up to £190 million in NPV terms.

…The paper presented [by the NAMA executive] to the [NAMA] Board projected the end-December 2013 carrying value of the loans at £1.48 billion. This was a forecast of the value of the loans that would be reported in NAMA’s 2013 annual financial statements.

However, the paper proposed a downward adjustment of £85 million in the carrying value to reflect additional expected impairment, resulting in an ‘adjusted carrying value’ of £1.39 billion. This examination found that the records supporting the December 2013 paper did not provide evidence justifying the adjustment.

Other evidence presented by NAMA during this examination supports a downward adjustment of, at most, around £8 million in cash terms. Consequently, the adjusted carrying value of £1.39 billion presented in the paper to the Board underestimated the value of the Project Eagle loans.

From page 12:

The NAMA paper for the Board recommended that the minimum price for the sale of the loans should be £1.3 billion, but did not state that this would represent the best achievable return, or what the recommended minimum price was based on.

From pages 12 and 13:

…the Board has stated that its decision on setting a minimum price was based on the portfolio’s adjusted carrying value (i.e. £1.39 billion) and on the Board’s acceptance that a purchaser’s discount of at least 10% would apply if the loan sale were to proceed. The Board also stated that the minimum reserve price was the best price deemed achievable through a loan sale.

…The argument that a discount rate of 10% would have been appropriate in calculating NAMA’s workout value for the loans is not persuasive.

From page 13:

The minutes of the meeting on 12 December 2013 record that: “The Board agreed that the paper and analysis presented therein presented a compelling commercial case to sell the portfolio, and that in addition such a portfolio sale would release NAMA from what had been a disproportionate burden of effort in light of the relative size of the portfolio.”

From pages 17 and 18:

During NIAC meetings and in annual statements of interests, one external NIAC member, Mr Frank Cushnahan, declared his involvement as an advisor, mainly on a non-fee basis, to six NAMA debtors and to a third party engaged in a joint venture with a seventh debtor.

The examination team estimated that the loans of the six debtors represented about half the value of the Northern Ireland loan book.

The NAMA Board should have formally considered whether Mr Cushnahan’s engagement in discussion of the strategy – including the PIMCO/Brown Rudnick approach – was consistent with his ongoing involvement as financial advisor to a significant proportion of NAMA’s Northern Ireland debtor connections.

…NAMA sought and relied on an assurance from Cerberus that no fee or payment was payable to anyone connected with NAMA “in connection with any aspect of our (Cerberus) participation in the Project Eagle sales process”.

NAMA only learned of Brown Rudnick’s engagement with Cerberus on 2 April 2014, and do not appear to have asked Cerberus when it engaged Brown Rudnick, or what was the precise nature of the services Brown Rudnick and Tughans were providing to Cerberus.

The allegations of Mr Cushnahan’s involvement in an arrangement to share fees with Brown Rudnick and Tughans (or the managing partner of Tughans) warranted more action by NAMA when the matter came to light, such as seeking advice from the unit within the National Treasury Management Agency that was responsible for providing compliance support to NAMA, or writing to Mr Cushnahan to seek confirmation or an explanation.

Lazard was not briefed on the disclosures, and was not asked for its assessment of the potential implications for the integrity of the sales process. NAMA appears to have taken a narrow approach, focusing on what were its legal obligations, rather than on what were the options for action that should be considered.

Meanwhile…

Look at how long it took to prepare Comptroller’s report. Govt would have known facts & draft conclusions since Jan pic.twitter.com/cNR49n4yld

— NAMAwinelake (@namawinelake) September 14, 2016

UPDATE:

.@NoelRock @SarahAMcInerney @chrisrdonoghue Actually, loss is €431m(£368m).That’s how much more NAMA could have got from working the loans

— NAMAwinelake (@namawinelake) September 14, 2016

@gavreilly Here’s the relevant para. NAMA had until 2020 to work out the loans & make £368m more than it sold for. pic.twitter.com/4UZr9x9xpv

— NAMAwinelake (@namawinelake) September 14, 2016

More as Namawinelake we reads it.

Read the report in full here

Waterford Independent Alliance TD John Halligan

Friday night.

On the Late Late Show on RTE One at 9.35pm.

Gareth Naughton writes:

Extreme adventurer Bear Grylls will chat about his wild life and putting Barack Obama through his paces… Waterford TD John Halligan will tell us how far he’s willing to go as the stand-off between him and his partners in Government continues… Dr Quinn Medicine Woman and Wedding Crashers star Jane Seymour drops by for a chat about life on- and off-screen…

…We’ll hear from Anna May McHugh about what’s in store for punters [at the Ploughing Championships] this year and Ivan Scott, world record sheep shearer, will demonstrate his skills live in studio.

…Entrepreneur Enda O’Coineen will talk about his passion for life on the waves as he prepares to take part in the Vendée Globe, a single-handed non-stop race around the world… BP Fallon talks about his rock ‘n’ roll life with the great and good of the music business including David Bowie and… he performs alongside Emmy Lou and the Agenda.

There will also music from Michael English and Vladimir & Anton.

Previously: Halligan’s Ball